Discover How We Can Help You Thrive

Thesis

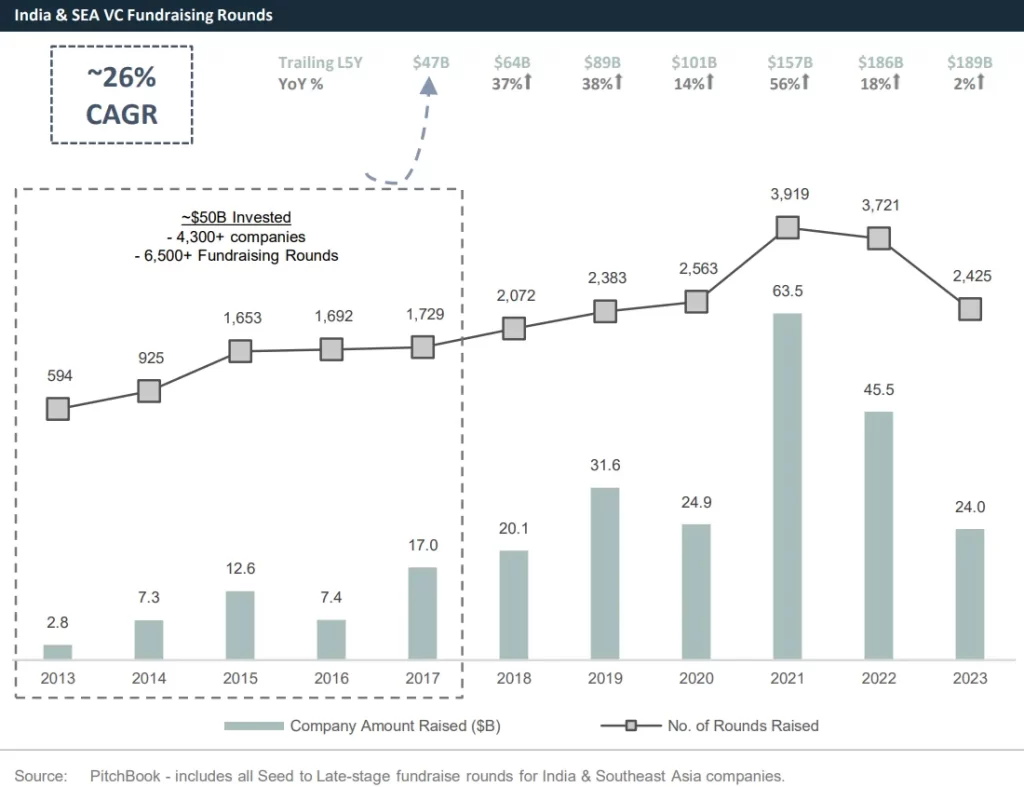

A multi-decade tailwind

Large & compounding

liquidity needs for past

deployed growth capital

Reimagining the Secondaries model

Invest in individual great companies at best availablerelative value

We look to invest into scaled market leader that are ~2-3 years to IPO who are profitable or havea clear path to profitability with a strong track record of managerial performance. We expect minimal dilution from subsequent private raises and look to underwrite at valuation levels that afford a margin of safety only because we believe in planning for the future vs. predicting it

Unique deal flow origination via proprietary networks

We seek to avoid buyer’s remorse by creating our own opportunities vs. participating in traditional broker-led auction processes that are shown to the entire buyer universe

Invest in individual great companies at best available

relative value

We view our investors as important partners in our franchise and believe in full alignment – in this case a whole-of-fund cash distribution to LPs before we even see a dollar of carry. In our house, LPs get served dessert before we even start on appetizers – this keeps us hungry to deliver superior risk-adjusted outcomes

Intelligent diversification via portfolio construction control

We eschew diversification for the sake of diversification. Instead we embrace intelligent diversification with a focus on curating our own portfolio weights, exposure and exit durations.

This means we cherry pick individual assets and avoid traditional secondary deals that result in a large basket with a long tail of unknown exposures, exit timelines and risks

Creating Win-win Outcomes

Company / Founders:

- Increase cap table alignment: reset holding period & raise weighted average cost basis (take out early investors) in preparation for IPO

- Value-add: add new active-management investors

- Cap table liquidity without disturbing primary valuation: provide ESOP, early investors with liquidity options

- Hassle-free process: no demanding informational needs on Company given familiarity of asset

Early Investors (Deep ITM):

- Realize carry: vs. rolling into continuation vehicle and delaying carry

- LP management: drive DPI today to support fund raising, LP conversations, etc.

- Release bandwidth: no need to continue managing assets in a large portfolio (~150+ investee companies)

- Hassle-free process: no need to go to LPAC (continuation vehicle), negotiate over multiple assets in a 6-18 month process with high degree of failure (marks move over time)

Total Body Fitness

MIND BODY

AND SOUL

Health

Lorem ipsum dolor sit alor amet, cotns ekolor adipiscing elit Nulla molestie convallis convallis.

nutrition

Lorem ipsum dolor sit alor amet, cotns ekolor adipiscing elit Nulla molestie convallis convallis.

GYM INCLUDED

Lorem ipsum dolor sit alor amet, cotns ekolor adipiscing elit Nulla molestie convallis convallis.

QUALITY

Lorem ipsum dolor sit alor amet, cotns ekolor adipiscing elit Nulla molestie convallis convallis.